Atal Beemit Vyakti Kalyan Yojana

Atal Beemit Vyakti Kalyan Yojana

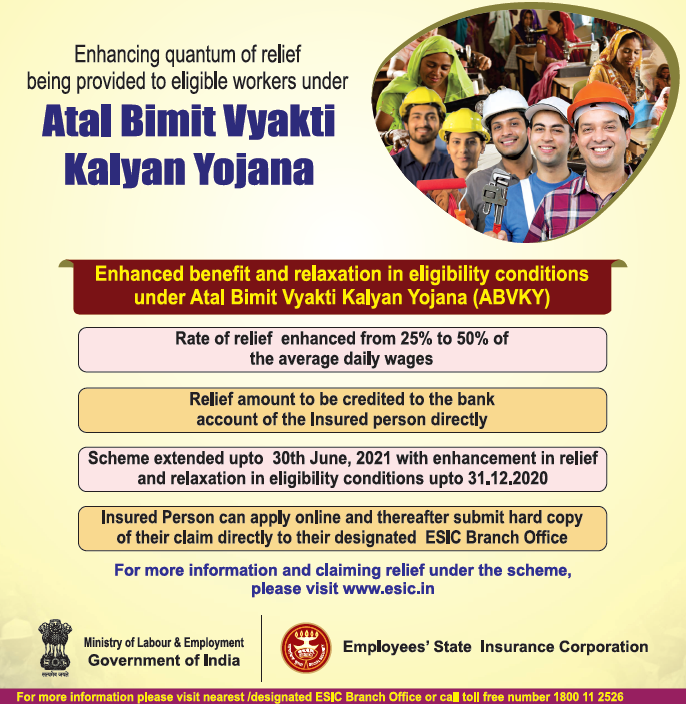

Atal Bimit Vyakti Kalyan Yojana is a welfare measure being implemented by the Employee's State Insurance (ESI) Corporation. It offers cash compensation to insured persons when they are rendered unemployed.

The Scheme was introduced w.e.f. 01-07-2018. The scheme is implemented on pilot basis for a period of two years initially. The scheme has been extended upto 20 June 2021.

Benefits under the scheme

The scheme provides relief to the extent of 50% of the average per day earning during the previous four contribution periods (total earning during the four contribution period/730) to be paid up to maximum 90 days of unemployment once in lifetime of the Insured Person.

Duration of allowance

- The maximum duration, for which an IP shall be eligible to draw the Relief under the Atal Beemit Vyakti Kalyan Yojana (ABVKY) will be 90 days once in life time after a minimum of two years of Insurable Employment and subject to the contributory conditions specified above. The claim for relief under the Atal Beemit Kalyaan Yojana will be payable after the three months of his/her clear unemployment. The relief will be paid for clear month of unemployment. No prospective claim will be allowed.

- In case the beneficiary gets gainful employment in between the three months of unemployment for which he was eligible for relief under ABVKY, the relief will be payable for clear month of unemployment between the date of unemployment and date of re-employment. The balance of 90 days of relief in this case may be claimed in the same manner as mentioned above based upon the initial contributory conditions by the beneficiary in case he again renders unemployed from Insurable employment within one year from initial unemployment.

Eligibility

- Employees covered under Section 2(9) of the ESI Act 1948.

- The Insured Person (IP) should have been rendered unemployed during the period the relief is claimed.

- The Insured Person should have been in insurable employment for a minimum period of two years.

- The Insured Person should have contributed not less than 78 days during each of the preceding four contribution periods.

- The contribution in respect of him should have been paid or payable by the employer.

- The contingency of the unemployment should not have been as a result of any punishment for misconduct or superannuation or voluntary retirement.

- Aadhar and Bank Account of the Insured Person should be linked with insured person database.

Other conditions for administration of the scheme

- In case the IP is working for more than one employer and is covered under the ESI scheme he will be considered unemployed only in case he is rendered unemployed with all employers.

- As specified in Section 65 of the ESI Act, an IP shall not be entitled to any other cash compensation and the Relief under ABVKY simultaneously for the same period. However, periodical payments of Permanent Disability Benefit (PDB) under ESI Act and Regulations shall continue.

- As specified under Section 61 of the ESI Act, an IP who is in receipt of Relief under ABVKY shall not be entitled to receive any similar benefit admissible under the provisions of any other enactment.

- The IP will be eligible for Medical benefit as provided under the Act for the period he is availing this relief.

Disqualification/Termination of relief under ABVKY

Relief under ABVKY shall not be admissible in the following circumstance:

- During lock out.

- Strike resorted to by the employees declared illegal by the competent authority.

- Voluntary abandonment of employment/ voluntary retirement/ premature retirement.

- Less than two years contributory service.

- On attaining the age of superannuation.

- Convicted (i.e. punished for false statement) under the provisions of Section 84 of the ESI Act read with Rule 62 of the ESI (Central) Rule

- On being re-employed elsewhere during the period he/she is in receipt of Relief under ABVKY.

- Dismissal/termination under disciplinary action.

- On death of IP.

Calculation of the relief amount

Illustration-1

Date of Unemployment : 01/04/2019

Contributory particulars of the preceding four contribution periods:

| Contribution Period | No.of Days | Wages |

|---|---|---|

| Oct 18 to March 19 | 182 | 60000 |

| April 18 to Sep 18 | 183 | 60000 |

| Oct 17 to March 18 | 182 | 60000 |

| April 17 to Sep 17 | 183 | 6000 |

| Total | 730 | 240000 |

Amount of relief/Benefit available for 90 days: (2,40,000/730) x (25/100) x 90 = Rs.7397/-

Ilustration-2

Date of Unemployment : 02/10/2018

Contributory particulars of the preceding four contribution periods:

| Contribution Period | No.of Days | Wages |

|---|---|---|

| April 18 to Sep 18 | 80 | 26667 |

| Oct 17 to March 18 | 183 | 60000 |

| April 17 to Sep 17 | 78 | 26000 |

| Oct 16 to March 17 | 78 | 26000 |

| Total | 419 | 138667 |

Amount of relief/Benefit available for 90 days:- (1,38,667/730) x (25/100) x 90 =Rs.4274/-

Submission of claim for relief

- To submit online claim, click here.

- The claim for Relief under ABVKY may be submitted by the claimant anytime after being rendered unemployed, but not later than one year from the date of unemployment to the appropriate Branch Office in form of affidavit in prescribed Form (AB-1). No prospective claim i.e. claim for relief under ABVKY for any future period will be allowed.

- The IP will submit his claim to his designated Branch office. A link for generating claim for Atal Beemit Kalyan Yojana will be given on the ESIC Portal. The Insured person will have to enter his insurance number, bank account number along with bank branch, Aadhar number, the period of claim, Bank account details and the mobile number on the page the above-mentioned link opens. The system after checking his eligibility will generate either (a) in case the IP is eligible for relief under ABVKY the claim in form AB-1 along with a forwarding letter from his last employer in form AB-2 and instruction for the IP OR (b) in case the IP is found not eligible, a regret message that the IP is not eligible for relief under the Atal Beemit Vyakti Kalyan Sarkari Yojana.

- The eligible Insured person will take the printouts of the claim submitted above and letter to the employer thus generated by the system and submit the duly signed claim in affidavit along with required forwarding by the employer to his designated ESIC Branch Office. Each claim thus generated will have an auto generated unique ID number.

- On receipt of the claim the details as mentioned by the applicant IP will be checked in the system by the staff at the Branch Office under supervision of the Branch Manager. The system will calculate the claimant's eligibility for relief under the scheme and its quantum for which the claimant is entitled based upon the details provided by the IP as well as the contribution and other details available in the system. The payment of the relief will be made to the IP's bank account.

Mode of payment

- The Relief under ABVKY shall be paid/ payable by Branch Office to IPs directly in their bank account electronically only. In the event of death of IP, the amount of Relief under ABVKY shall be paid/ payable to his/her nominee/legal heir as prescribed under Para(s) P.3.79.1 to P.3.81 of the Branch Office Manual by the account payee cheque only.

- The bank account details of the claimant in the ESIC Database is a pre-condition for claiming this relief, but in case the bank account details of the claimant are not available in the ESIC Database or the IP has changed his bank account then the same may be authenticated by the Branch Manager on the basis of the canceled cheque leaf or the passbook of the bank account having name of the claimant on it, which the claimant will provide along with the claim for this relief. The claim shall be processed on AB-3.

To view the FAQs abou the scheme, click here.

Claim process under Atal Beemit Vyakti Kalyan Yojana further liberated

Atal Beemit Vyakti Kalyan Yojana of ESI Corporation provides relief in form of cash compensation to Insured Persons in the contingency of their unemployment. Presently under this Scheme 50% of average earning of the Insured Person ispaid for maximum 90 days in case of his unemployment subject to certain contributory conditions.

It was brought to the notice of ESIC that in some cases employers have struck off their employees from the rolls few months after actually terminating them from service. During this period, ESI contribution was also not filed by the employers for these employees in the system. As the relief under Atal Beemit Vyakti Kalyan Yojana is available only in case of unemployment of the Insured Persons, such. employees though terminated from service became ineligible for relief under this scheme.

The matter was reviewed and ESIC has now decided that in cases where the employer has shown "Zero" contribution in respect of an employee for some months before exiting him from the system, the relief under ABVKY for such period of "Zero" contribution, shall also be allowed. However, only those beneficiaries who have been exited from the rolls of the employer, shall be considered for payment of relief under ABVKY subject to fulfilment of other eligibility conditions.

Last Modified : 12/17/2021

This topic provides information about Employees’ S...

This topic provides information about "Frequently ...

This topic contains the information related to Aam...

Information related to online Public Grievance red...